You are here

What U.S. and Foreign Officials Have Said About The Fed's Activities in the Gold Market - Bill Murphy

From the transcript of the minutes of the Federal Open Market Committee on March 26, 1991 (www.federalreserve.gov/fomc/transcripts/1991/910326Meeting.pdf): Near the end of a lengthy discussion (pp. 8-21) of U.S. foreign exchange reserves, which are held in approximately equal portions by the Fed and the Exchange Stabilization Fund, former Fed governor Wayne Angell added (p. 19):

There's one slight addendum to this discussion: ... [I]f you mark our gold to the $358 price, we end up with something like $170 billion [in total foreign exchange and gold reserves]. There are opportunity costs because we don't get interest on that gold as we do on our foreign exchange [holdings]. That cost is out there also. I would hesitate for us to have foreign currency holdings that have swap puts that just sit there, [which] is now becoming the case for our gold. [Emphasis supplied.]

From the transcript of the Federal Open Market Committee meeting on January 31, 1995 (www.federalreserve.gov/fomc/transcripts/1995/950201Meeting.pdf): Responding to a question raised by then Federal Reserve Board Governor Lawrence Lindsey about the legal authority of the ESF to engage in the financial rescue package for Mexico then under discussion, J. Virgil Mattingly, general counsel of the Fed and FOMC, stated (p. 69):

It's pretty clear that these ESF operations are authorized. I don't think there is a legal problem in terms of the authority. The statute [31 U.S.C. s. 5302] is very broadly worded in terms of words like 'credit' -- it has covered things like the gold swaps -- and it confers broad authority. Counsel at the White House called the Treasury's General Counsel today and asked "Are you sure?" And the Treasury's General Counsel said "I am sure." Everyone is satisfied that a legal issue is not involved, if that helps. [Emphasis supplied.]

Note: As described by the FOMC (www.federalreserve.gov/fomc/transcripts), transcripts of its meetings in 1995 were prepared "shortly after each meeting from an audio recording" and "[m]eeting participants were then given an opportunity within the next several weeks to review the transcript for accuracy." Nevertheless, in a memorandum dated June 8, 2001, to Chairman Greenspan (and later released by him to Senator Jim Bunning, Kentucky) (http://groups.yahoo.com/group/gata/message/827), Mr. Mattingly disclaims his 1995 statement about gold swaps, stating in relevant part:

Given the passage of time, some six years, I have no clear recollection of exactly what I said that day but I can confirm that I have no knowledge of any "gold swaps" by either the Federal Reserve or the ESF. I believe that my remarks, which were intended as a general description of the authority possessed by the Secretary of the Treasury to utilize the ESF, were transcribed inaccurately or otherwise became garbled.

From U.S. Treasury Directive TD 27-04 (www.ustreas.gov/regs/td27-04.htm), dated November 17, 1996, describing the functions of the Office of Under Secretary (International Affairs) and the duties of the Deputy Assistant Secretary (International Monetary and Financial Policy) (part 5.h):

Provides direction to the Federal Reserve Bank of New York concerning Exchange Stabilization Fund (ESF) operations under the authority of the Secretary of the Treasury and other Treasury officials who are delegated such authority to assure that operations of the Federal Reserve System concerning the ESF are coordinated. In this regard, the incumbent intensively monitors foreign exchange markets and maintains continuing monitoring of gold markets and related developments. [Emphasis supplied.]

Note: This directive, which expired November 17, 1999, appears in virtually identical form as a current directive under the Assistant Secretary (International Affairs) (www.ustreas.gov/org/dasimfp.htm).

From testimony of Fed Chairman Alan Greenspan before the House Banking Committee and Senate Agricultural Committee in July 1998 (http://agriculture.senate.gov/Hearings/Hearings_1998/gspan.htm):

Nor can private counterparties restrict supplies of gold, another commodity whose derivatives are often traded over-the-counter, where central banks stand ready to lease gold in increasing quantities should the price rise. [Emphasis supplied.]

From Chairman Greenspan's letter to Senator Joseph I. Lieberman, Connecticut, dated January 19, 2000, elaborating upon the foregoing testimony (http://groups.yahoo.com/group/gata/message/346):

This observation simply describes the limited capacity of private parties to influence the gold market by restricting the supply of gold, given the observed willingness of some foreign central banks -- not the Federal Reserve -- to lease gold in response to price increases. [Emphasis supplied.]

From the same letter by Chairman Greenspan:

The Federal Reserve owns no gold and therefore could not sell or lease gold to influence its price. Likewise, the Federal Reserve does not engage in financial transactions related to gold, such as trading in gold options or other derivatives.

Most importantly, the Federal Reserve is in complete agreement with the proposition that any such transactions on our part, aimed at manipulating the price of gold or otherwise interfering in the free trade of gold, would be wholly inappropriate.

From the Complaint in Howe v. Bank for International Settlements, et al., United States District Court for Massachusetts, No. CV-00-12485-RCL (http://www.goldensextant.com/Complaint.html): The reaction of the Fed and other central banks to the sharp rally in gold prices triggered by announcement of the so-called "Washington Agreement on Gold" in September 1999, as described by Edward A. J. George, Governor of the Bank of England and a director of the BIS, to Nicholas J. Morrell, then Chief Executive of Lonmin Plc, a principal shareholder in Ashanti Goldfields Ltd. (paragraph 55):

We looked into the abyss if the gold price rose further . A further rise would have taken down one or several trading houses, which might have taken down all the rest in their wake. Therefore at any price, at any cost, the central banks had to quell the gold price, manage it. It was very difficult to get the gold price under control but we have now succeeded. The U.S. Fed was very active in getting the gold price down. So was the U.K. [Emphasis supplied.]

LOOKING INTO THE ABYSS: GOLD AND INTEREST RATE DERIVATIVES

The "abyss" was the problem of covering the short physical gold position evidenced by a mountain of gold derivatives on the books of the bullion banks.

Central banks put physical gold from their vaults into the market by outright sales or by leasing, which may include not only gold loans but also gold deposits or swaps with major bullion banks. Technically different but functionally the same, gold on lease, deposit or swap is reported by most central banks as part of their gold reserves. However, the physical gold itself is ordinarily sold into the market by the bullion banks receiving it, resulting in a short physical position, meaning that the gold ultimately required for repayment must be purchased in the market or obtained from new mine production. The bullion banks are intermediaries, they borrow central bank gold at low rates [1-2%], sell it at spot for cash, put the cash into financial assets earning higher returns [e.g., 5%], and generally hedge their short position by going long in the forward market. Leading U.S. bullion banks include J.P. Morgan Chase, Citibank and Goldman Sachs; leading overseas bullion banks include Deutsche Bank and UBS.

When bullion banks go long, someone else in the forward market must go short because all contracts in that market have two sides, buyer and seller. This hedging produces gold derivatives, e.g., forward contracts, options. Who goes short in the forward market? Gold producers hedging future production; jewelers hedging inventory; speculators. Shorts in the forward market typically also earn a contango, which is almost but not quite equal to the spread earned by the bullion bank. The bullion bank has a hedged position on which it earns a small margin [0.5%]. Shorts in the forward markets are the ultimate gold borrowers, but the bullion banks are the ultimate guarantors of gold repayments to the central banks.

Pursuant to rules promulgated by the IMF (http://groups.yahoo.com/group/gata/message/904), central banks are not required to report gold in the vault separately from gold receivables on account of gold loans, deposits or swaps. Accordingly, there are no authoritative reported numbers from which to calculate the total short physical position. Credible estimates run from around 5000 metric tonnes to over 15,000 tonnes out of total reported central bank gold reserves of roughly 32,000 tonnes. Annual demand is estimated at 4000 to 4700 tonnes, leaving a deficit of 1500 to 2200 tonnes to be filled by scrap, official sales, and gold leasing mostly by central banks.

In May 2000, five delegates from GATA (http://www.gata.org/index.html) made a 45-minute presentation to House Speaker Dennis Hastert on the dangers to the U.S. financial system posed by the exploding quantities of gold derivatives on the books of the bullion banks as a result of gold leasing by central banks. In this connection, GATA published an advertisement (www.goldworld.net/rollcall.htm) in Roll Call, the congressional newspaper, and delivered an extensive written document, Gold Derivative Banking Crisis (www.gata.org/test.html), to every member of the House and Senate banking committees. Within the next six months, more than 20,000 copies of Gold Derivative Banking Crisis were downloaded from the GATA site.

Why do central banks loan gold? The reason most frequently cited is a desire to earn a return, however paltry, on an otherwise "sterile" asset. But as Chairman Greenspan suggested to Congress in 1998, the real reason usually has much more to do with suppressing gold prices. In 1988, Harvard president and former U.S. treasury secretary Lawrence H. Summers, then Nathaniel Ropes professor of political economy at Harvard, co-authored with Robert B. Barsky an article entitled "Gibson's Paradox and the Gold Standard" published in the Journal of Political Economy (vol. 96, June 1988, pp. 528-550). A principal conclusion of the article is that in a genuinely free gold market unaffected by "government pegging operations," gold prices will move inversely to real long-term interest rates, rising when real rates fall, and falling when real rates rise.

A commentary on this article published in August 2001 at The Golden Sextant (http://www.goldensextant.com/commentary18.html) includes the chart reproduced below depicting real long-term interest rates (30-year T-bond yield minus 12-mos. cumulative CPI) and gold prices (inverted) since 1977. As the commentary points out:

"Gibson's paradox continued to operate for another decade after the period covered by Barsky and Summers. But sometime around 1995, real long-term interest rates and inverted gold prices began a period of sharp and increasing divergence that has continued to the present time. During this period, as real rates have declined from the 4% level to near 2%, gold prices have fallen from $400/oz. to around $270 rather than rising toward the $500 level as Gibson's paradox and the model of it constructed by Barsky and Summers indicates they should have.

"The historical evidence adduced by Barsky and Summers leaves but one explanation for this breakdown in the operation of Gibson's paradox: what they call 'government pegging operations' working on the price of gold. What is more, this same evidence also demonstrates that absent this governmental interference in the free market for gold, falling real rates would have led to rising gold prices which, in today's world of unlimited fiat money, would have been taken as a warning of future inflation and likely triggered an early reversal of the decline in real long-term rates."

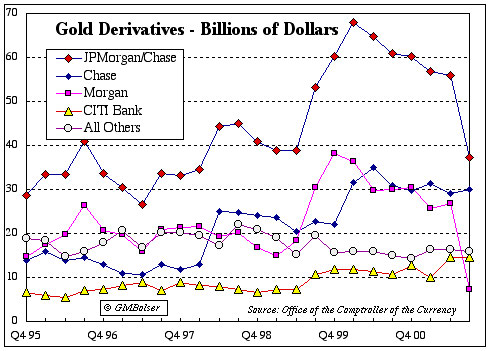

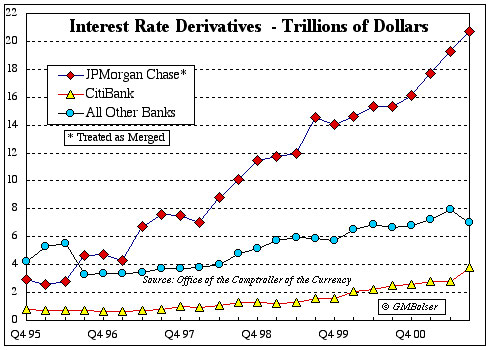

What new alchemy drove real long-term rates and gold prices lower together after 1995? The next two charts, also from The Golden Sextant (http://www.goldensextant.com/Charts.html), depict the notional values of gold and interest rate derivatives as reported quarterly to the Office of the Comptroller of the Currency by U.S. commercial banks since 1995. Of particular note are: (1) the sharp rise in Morgan's gold derivatives in the last two quarters of 1999; (2) the sharp rise in Chase's gold derivatives in the first two quarters of 2000; (3) the massive cumulative totals for the new J.P. Morgan Chase, which as a result of the merger approved by the Fed in December 2000 now holds almost two-thirds of all gold and all interest rate derivatives on the books of U.S. commercial banks; and (4) the sharp drop in the still separately reported gold derivatives of Morgan in the third quarter of 2001 while those of Chase, Citibank and All Other remained static.